State Insurance News

Proposed Fla. Legislation Aims to Bring Insurance Premiums to Heel for Multi-Unit Condos

Twin bills in Tallahassee would reduce costs by allowing for depreciated or cash-value roof coverage

The Champlain Towers South in Surfside, just north of Maimi Beach, Fla., was a 12-story beachfront condominium that partially collapsed just after 1 a.m. in June 2021, killing 98 and becoming one of the worst structural failures in American history. The disaster was followed by a brutal hurricane season. One of the results of these twin disasters was a wholesale vacating of most commercial insurance companies writing insurance policies in Florida.

— Photo Courtesy of Engineering News-Record

Florida’s insurance woes have been well documented in the pages of this magazine, and the latest legislative fix involves a proposal revising windstorm insurance coverage payments that would make premiums more affordable for the state’s countless condominium buildings if the bills become law.

The bipartisan legislation, moving consecutively in both chambers of the state legislature, would create a pilot program requiring state-owned Citizens Property Insurance Corp. to cover roofs of condo buildings at actual cash — also known as depreciated — value rather than at full replacement cost.

Depreciated value is the minimum amount an asset is worth after “depreciation”; depreciation is the decrease in an asset's value over time due to wear and tear, use, obsolescence, or other factors.

The bill’s sponsors, Sen. Ana Maria Rodriguez (R-FL 40) and Rep. Hillary Cassel (D-FL 101) believe the program, which the Office of Insurance Regulation would create, could eliminate situations where buildings’ condo boards fail to find coverage or go without full coverage due to rising costs, which puts its residents in potentially calamitous financial peril.

In one instance, first reported by the South Florida Sun-Sentinel on Dec. 9, a man who was selling his late mother’s condo in a sprawling complex in Sunrise, Fla., got a rude awakening after a potential buyer was denied a mortgage after the lender discovering the condo association’s insurer canceled its windstorm policy in the middle of this year’s hurricane season.

The Sun-Sentinel cited the association’s treasurer as saying that the roofs had reached the end of their “useful life” but were not scheduled to be replaced until the following year; the association decided to forego finding new coverage and decided it would use the reserve money for repairs if necessary.

Basically, the association decided to take a risk and got lucky this past hurricane season as no significant storm hit South Florida. Still, the homeowner in the story took a $40,000 haircut on the sale price of the condo because of the failure of the condo board to have full wind insurance coverage.

The legislators, whose districts cover large swaths of Southeast Florida’s two most populated counties, Broward and Miami-Dade, did not provide comment on the legislative proposals; Rodriguez’s spokesman, Luke Strominger, issued a statement explaining that the proposed pilot program is intended “to reduce insurance costs and increase choices for condo associations.”

Should the legislation pass, eligibility would require majority votes by condominium association members, and the association would have to conduct roof inspections every two years.

Critically, the bills would also require that the cash value of the insured roof “align with reserves” as required by Florida’s condominium law; in other words, the cash reserves must cover the remainder of the cost of a new roof after Citizens pays an actual cash value or ‘depreciated’ claim.

The cash reserve requirement is a crucial element of the bill that would help insulate the state’s many roofing contractors since insurance repair is a substantial part of many roofing firms' businesses.

Insurance is Great If You Can Get It

It’s been reported that many large, multimillion-dollar condominium complexes have been hit hard by the ongoing insurance crisis as private carriers leave the state, which was exacerbated by the collapse of the Champlain Towers in Surfside in June 2021.

It’s been reported that many large, multimillion-dollar condominium complexes have been hit hard by the ongoing insurance crisis as private carriers leave the state, which was exacerbated by the collapse of the Champlain Towers in Surfside in June 2021.

The few private-market companies willing to cover large complexes have raised premiums substantially, and the result has been steep increases in condo association fees that have left owners, often retirees, facing untenable costs.

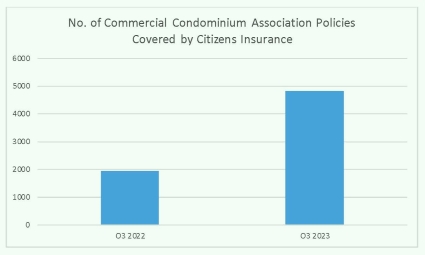

As a result, Citizens, the Sunshine State’s insurer of last resort, experienced significant growth in the number of commercial condo policies and value of covered condo properties in the third quarter of 2023 compared to the previous year.

According to data released by the Florida Office of Insurance Regulation, the number of commercial condo policies covered by Citizens increased by 148% — from 1,947 to 4,824 — during that time.

In financial terms, the dollar value of covered properties more than tripled — from $17.6 billion to $78.6 billion, while premiums collected for those policies went up by nearly five times — from $117.3 million to $666.9 million.

Citizens spokesman Michael Peltier told the Sun-Sentinel last month that there was a disproportionate rise in covered property value and premiums to an increase in the number of buildings it insures with a replacement value of $10 million or more. The increase resulted from the trouble many condo associations had securing full limits for wind coverage.

The proposed legislation also allows insurance premiums through Citizens for buildings valued at $10 million or more to be uncapped versus a ceiling for individual homeowners using the state insurer.

The pilot program created by the twin bills would not go into effect until July 1 next year and would last through 2029. Of course, that means associations would need to secure wind coverage under current conditions for at least one more year; hurricane season officially begins on June 1.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

Bryan Gottlieb is the online editor at Engineering News-Record (ENR).

Gottlieb is a five-time Society of Professional Journalists Excellence in Journalism award winner with more than a decade of experience covering business, construction, and community issues. He has worked at Adweek, managed a community newsroom in Santa Monica, Calif., and reported on finance, law, and real estate for the San Diego Daily Transcript. He later served as editor-in-chief of the Detroit Metro Times and was managing editor at Roofing Contractor, where he helped shape national industry coverage.

Gottlieb covers breaking news, large-scale infrastructure projects, new products and business.

![]()

email gottliebb@enr.com | office: (248) 786-1591

.webp?height=740&t=1781278983&width=auto "KEE(2).png")