Year 2001 Economic Forecast

Another great year for Roofing Contractor readers! That is how I would characterize the year 2000. Economic growth and increases in productivity remained solid. The construction industry remained very healthy. The big negative was the very volatile stock market and especially the losses experienced on the tech-weighted NASDAQ. To provide you with an economic forecast for 2001, I consulted with David Orr, senior vice president and chief economist for First Union Capital Markets Corp., Charlotte, N.C. Orr provided substantial input for this article as well as the accompanying charts.

This forecast is divided into three parts. The first provides a broad overview of the economy, examining trends in economic growth, inflation and interest rates. This sets the stage for the second part, a discussion of specific trends in the construction industry. The third part provides a discussion and suggests trends for the stock market in 2001.

The Macro Outlook

It’s time to sober up. Nirvana is over — at least for a while. In fact, a number of doomsayers are actually predicting a recession for 2001. We do not foresee a recession and most members of the construction industry have not yet experienced anything that would suggest a slowdown from the past couple of years. However, we are at more risk now for a decrease in consumer spending, an increase in unemployment and a cooling of the construction market than during the past few years. (If consumer spending did decrease and unemployment started to increase, the Federal Reserve Bank would likely reduce short-term interest rates and stimulate economic growth to prevent a recession.)Economic growth during 2000 continued to be exceptionally strong and will probably be 5 percent for the year (see Figure 1). The rate of economic growth is starting to decline, however — returning to more normal levels of 2.5 to 3.0 percent. This change will require a temporary adjustment period and we foresee a slowing of vehicle starts and housing starts, for example. Durable goods orders are already slowing and the price of lumber is plunging. Clearly, we are seeing an inventory overhang in durable goods (witness the number of automotive rebate programs). During the early fall, 183,000 jobs were lost in manufacturing. Furthermore, there has not been a net increase in construction jobs during the past six months. When the final numbers are calculated, we anticipate a 3.3 percent annualized real economic growth rate in the fourth quarter of 2000 and then 3.6 and 3.0 percent growth rates for 2001 and 2002 respectively.

Business owners are cautioned not to bask in the glow of the past two years. Rather, we encourage you to look back at your profit and loss statements from 1996 and 1997 — the two years before the start of the frenzied growth of 1998 to 2000. Base your business plans for 2001 on the kind of growth experienced during 1996 and 1997 rather than the past two years.

Looking longer term, we are optimistic. The ongoing investments in technology and employees as well as enhanced global competition have contributed to increased productivity. These long-term structural changes set the stage for sustained periods of real economic growth (perhaps at a 4 percent annual level) with moderate inflation. This is very good news.

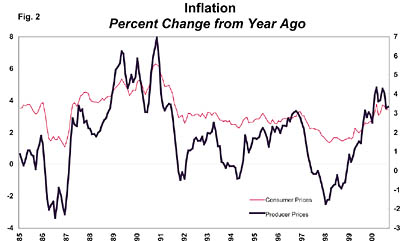

Inflation and Interest Rates

The very strong economic growth during 2000 resulted in decreasing unemployment and that is translating into higher labor costs. Increasing labor costs have been partially offset by unusually high gains in productivity. The rate of increase in productivity will likely start to abate, however. Furthermore, the low cost of oil (remember when it was $10.00 a barrel) that helped hold inflation in check is now only a memory. Consequently, when the calculations are complete, we see inflation as measured by the Consumer Price Index for 2000 at about 3.3 percent and increasing to as much as 4 percent over the winter. This contrasts with 1.6 and 2.2 percent for 1998 and 1999 respectively (see Figure 2). The rate should slow to about 2.7 percent as the economy cools during the latter part of 2001.Interest rates are driven largely by the actual and anticipated rates of inflation. A primary goal of the Fed is to hold inflation in check, which it does by increasing short-term interest rates when higher rates of inflation are anticipated. For example, we witnessed several Fed short-term interest increases during 2000 designed to cool the economy and thereby reduce inflationary pressures. We do not foresee significant short-term interest rate changes during 2001. In the event that unemployment starts to increase, however, then the Fed may lower short-term rates (see Figure 3).

Bond traders primarily control long-term interest rates (such as those on the 10-year Treasury notes that serve as a basis for mortgage interest rates). When bond traders perceive higher inflation, they bid upward bond interest rates. During 2000, budget surpluses resulted in the Treasury reducing the amount of federal debt. This helped to keep long-term rates from increasing significantly. Furthermore, with the lofty projections of future surpluses, some bond traders were willing to accept lower interest rates on Treasury bonds because they anticipated a possible shortage of them in the future. Now, with the prospect of higher government spending and/or tax rate reductions, the possibility for surpluses is evaporating and so is the concern about shortages of Treasury bonds. Finally, with the extreme volatility in stock prices, traders took a “flight to quality” (purchased Treasury notes and bonds). That tended to moderate longer-term interest rates. Looking to 2001 we see mortgage rates in the 7 to 8 percent range, an increase from the recent lower rates of 7 5/8 percent.

The Residential Housing Market

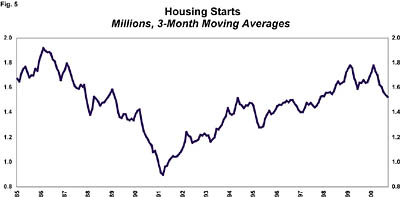

New home construction increased significantly over the past few years. During 1998, new housing starts were 1.66 million units and remained virtually unchanged through 1999. This level of new home starts is significantly above the level that can be supported by new family formations — the underlying driving force in new home construction.We saw the level of new housing starts decrease during the end of 2000 to an annual rate of about 1.5 million units. Looking ahead, we expect the rate to decrease to an annual rate of about 1.45 million units during the first half of 2001. By most historical standards, however, 1.45 million housing starts would be considered quite strong. Similarly, we expect existing home sales to drop from the current 5 million level to a more sustainable 4.5 million level.

The level of new home construction may increase slightly to perhaps 1.5 million in the next few years as the recent wave of immigrants purchase homes. Furthermore, the population of 25-35 year olds (the primary first-time homebuyers) will start to increase in about five years providing another small boost to housing starts. Finally, the first wave of the large population of extremely affluent baby boomers who can afford to live wherever they want in retirement will turn 55 in 2001. We therefore continue to anticipate increasing demand for property in the traditional retirement states as well as in shore areas.

The anticipated decrease in housing starts to the 1.45 million level is in keeping with the rate of family formations. The 1998-1999 surge in housing starts resulted from several factors. First, there was the surge in stock market prices. People felt wealthy and built new homes. Stock market gains changed to losses in 2000; the wealth effect may be on hold! Second, the 1997 tax law changes that permit a $500,000 exclusion in home sales capital gains as frequently as every two years spurred a spike in construction. Third, mortgage rates plunged, dropping from 9 percent in the fall of 1997 to 6.5 percent in the fall of 1998. Now rates are higher and another precipitous drop is very unlikely. Finally, job growth was extremely strong during the past two years and spurred new home sales. With very low unemployment rates, job growth will slacken. We caution readers not to expect the level of expansion seen in 1998 and 1999. Plan to be more cautious during 2001(see Figures 4 and 5).

Nonresidential Construction

While residential construction is expected to decline during 2001, non-residential construction is expected to grow. Nationally, office vacancy rates are low — averaging about 6 percent. Office construction grew 8 percent during 2000 and should continue to grow during 2001. The weak link in nonresidential construction is industrial facilities — down about 25 percent over last year and expected to decrease even more during 2001. The decrease results from over capacity and higher energy prices that are eroding profits. This is a reflection of the worldwide over capacity in production facilities and energy costs. Also, we do not anticipate significant growth in retail facilities.The forecast for school construction remains very solid. As states continue to enjoy budget surpluses and the federal government exhibits increasing interest in education, school construction and retrofitting should remain solid for the next five to 10 years.

Hotels and motels continue to be overbuilt, particularly the mid-price range units along the interstates. Currently, construction in this sector is expected to decline. By contrast, upscale downtown hotels are experiencing higher occupancy rates and construction of these facilities should continue (see Figure 6).

Stock Market Outlook

During the five-year period from 1995 through 1999 the S&P 500 stock average (an average of 500 large companies) increased nearly 29 percent a year — spectacular growth. Things turned south in 2000, and especially for many high-tech NASDAQ stocks. Looking back, 1999 may be viewed as a pivotal year. While many major market indices increased appreciably due to the heavy weighting of very large capitalization companies in those indices, the typical stock of the approximately 7,000 U.S. stocks listed on the various exchanges decreased about 15 percent. Actually from mid 1998 to the start of 2000, we had a bear market in about 2/3 of stocks. But this was masked by the increasing prices of large-cap companies. During 2000, many of the small- and mid-cap stocks increased in value while the large-cap stocks have tended to take a beating.What lies ahead? Stock prices are driven largely by current and anticipated profits, changes in interest rates (lower interest rates generally lead to higher stock prices), the level of investor exuberance, and the flow of money into the stock markets. With the slowing rate of economic growth and higher employment and energy costs, the chances for significant earnings increases during 2001 are slim. Furthermore, we do not expect interest rates to fall very much during 2001. Investor exuberance has waned since the NASDAQ took a dive; many investors are scared. On the plus side, billions continue to flow into the stock markets each month largely from individual retirement accounts, 401(k) and other retirement plans. For many investors the stock market is the only game in town and this ongoing inflow of funds will tend to buoy the market or keep it from sinking rapidly.

For 2001 we expect profits to grow only about 5 percent (as contrasted with 10 percent in 2000). Therefore during 2001 we anticipate little if any stock market growth or loss — with the broad market measures likely increasing or decreasing by about five percent. We foresee further investor adjustment to realistic earnings expectations.

Most readers are in the market for the long run — often with 30, 40 or 50-year retirement planning horizons. History indicates that those who invest regularly and do not attempt to time the markets come out ahead. So, we don’t recommend jumping ship. However, investors should diversify their stock portfolios to include small- and mid-cap as well as large-cap companies. Also investing selectively in international stocks, perhaps 20 percent in small- and mid-cap companies and 20 percent in international stocks, should be considered. This year’s favorite is likely to be next year’s ugly duckling. Diversify, diversify, diversify!

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

.webp?height=740&t=1781278983&width=auto "KEE(2).png")