Guest Column

Basu: High Rates, Costs Challenge Construction Growth

Economist highlights inflation, rates and sector divides

Before leaders of the metal building industry in Colorado Springs, Colo., keynote speaker Anirban Basu, a respected industry economist, underscored both the opportunities and headwinds facing construction: the U.S. economy is still growing, but growth is increasingly uneven, and industry professionals need to be clear-eyed about where opportunity exists and where risk is building.

Speaking at the joint Metal Building Contractors and Erectors Association/Metal Building Manufacturers Association (MBCEA/MBMA) event, Basu offered an early roadmap to the financing, labor, inflation and market questions facing the metal construction industry — conversations that will carry into METALCON 2026, where thousands of metal construction professionals will gather amid ongoing discussion about the market forces shaping the year ahead.

Basu, chief economist for the Associated Builders and Contractors, the Construction Financial Management Association and the Modular Building Institute, and a former chair of the Maryland Economic Development Commission, brought a practical, construction-focused perspective to the stage. His core point was blunt: the economy is growing, but the benefits are uneven. “So, it’s a lopsided economic expansion with some families really benefiting, and other families really fading in terms of standard of living,” Basu said.

Source: Board of Governors of the Federal Reserve System (US) via FRED. Courtesy of METALCON.

Source: Board of Governors of the Federal Reserve System (US) via FRED. Courtesy of METALCON.Prices, Rates and Project Pressure

One of Basu’s clearest messages centered on inflation and the frustration it is creating. He said there is “a fair amount of angst out there regarding the economy,” as well as “a fair amount of unhappiness” and “a significant amount of discontent,” driven in part by rising everyday costs such as groceries. At the heart of that discontent, he said, is “high and rising prices.” He noted that overall inflation has climbed 29% since May 2020, while core inflation has risen 25.7% over the same period.

That matters because inflation continues to keep interest rates elevated, raising the cost of capital and making many projects harder to pencil. Basu noted that after holding its benchmark rate near zero early in the pandemic, the Federal Reserve raised it to about 5.5% before later easing, but borrowing costs remain high relative to the pre-pandemic environment.

As he put it, “Borrowing costs go up, project financing costs go up. That’s not good for construction projects.” Basu said inflation is likely to linger, keeping interest rates higher for longer — an unwelcome outlook for the construction industry, which needs private financing costs to come down to support more construction starts.

That pressure is most visible in residential construction and parts of the commercial market. Basu pointed to declining housing under construction, weak permit activity and continued softness in multifamily, where many projects are simply not viable at today’s financing and input-cost levels.

He also emphasized that the office sector remains a weak spot, with remote and hybrid work continuing to weigh on vacancy in major metropolitan areas, putting pressure on property values, lender appetite and municipal tax bases. As a result, private-sector work tied to traditional office, speculative multifamily and other rate-sensitive development remains under strain.

Where Strength Is Concentrated

At the same time, Basu made clear that not all construction sectors are struggling. He singled out data centers and the energy generation and distribution infrastructure needed to support them as two of the strongest opportunities ahead. “These two segments of construction tend to be the strongest going forward,” he said.

He described artificial intelligence as one of the defining drivers of capital spending in today’s economy, with hyperscalers, such as Amazon and Meta, spending about $450 billion last year on related architecture and infrastructure and expected to spend $700 billion to $725 billion this year. He also noted that data centers used about 4.4% of U.S. electricity in 2023 and could consume well above 12% by 2028. Those trends will keep driving demand for power generation, transmission and related utility work, while also reinforcing the appeal of fast-track, durable building systems.

Public construction is another relatively bright spot. Basu showed that while total nonresidential construction has flattened, infrastructure-related categories such as transportation, water supply, sewage and waste disposal, and conservation-related work continue to benefit from public funding already moving through the system. In practical terms, that means companies with exposure to civil, utility and public-sector work may find better near-term stability than those dependent on speculative private development.

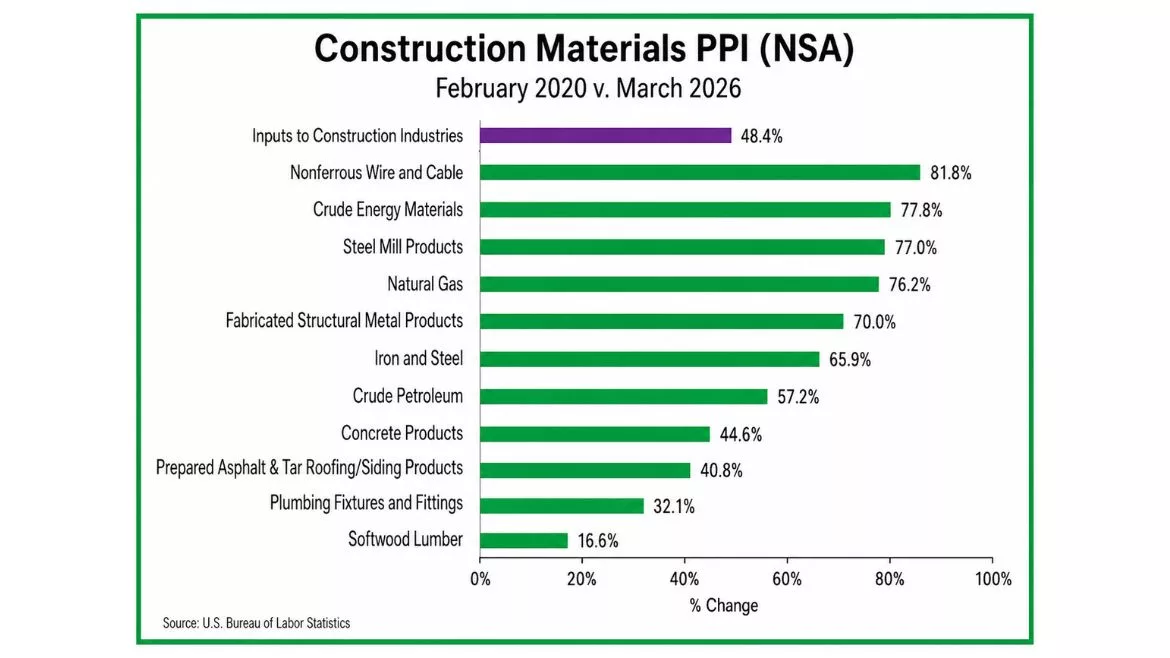

Materials Costs Remain a Problem

Basu underscored rising construction input costs, particularly in metals-related categories. He said construction materials prices overall were up 48% from February 2020 to March 2026. The more targeted figure may be even more important: Basu said the producer price index – the price received by producers – for architectural and structural metals manufacturing was up 7.4% year over year and 75% since February 2020. He also pointed to steep increases in steel mill products and fabricated structural metal products, highlighting how tariff policy and supply-side pressures continue to affect pricing.

Materials volatility continues to shape pricing, bidding, procurement strategy and project timing. In a market where owners are already struggling with financing, further escalation can push work from delayed to dead.

Labor and Location Still Matter

Labor remains another complicated piece of the outlook. Basu noted that construction job openings have not surged the way some expected, even with changes in immigration policy affecting workforce availability. He said about 25% of the construction workforce is foreign-born, but the expected increase in advertisements for native-born or documented workers has not materialized. The reason, he suggested, is that between residential and nonresidential construction, overall construction spending has been in decline, even though some individual segments continue to grow. That means labor availability, wage pressure and productivity remain key concerns, particularly in labor-intensive trades. Even where demand exists, execution still depends on workforce access and retention.

Basu also urged the audience to think regionally, not just nationally. Some markets can transcend a weakening economy, particularly when population growth continues to drive demand. Economic momentum remains strongest in places that continue to attract people and business investment, including parts of Texas, Florida and the Carolinas. Those regions are more likely to support job creation and construction demand. Markets dealing with population outflows, weak office fundamentals or fiscal strain face a more difficult path.

What Comes Next for Metal Construction

As the industry looks ahead to METALCON 2026, the same questions Basu raised continue to shape conversations about where work is coming from, which projects still pencil and how companies can position themselves for the next phase of the cycle. Strength remains concentrated in a relatively narrow group of drivers – artificial intelligence spending, data centers, power infrastructure and public work – while other parts of the market remain constrained by financing costs, input prices and softer demand.

In closing, Basu said, “So there are four things I’m watching to determine whether or not we’re going to enter recession.” First is the conflict in the Middle East, which he said the stock market appears to be treating as temporary, even though “it hasn’t ended yet, and things can go wrong.” Second is hyperscaler spending, particularly what major technology companies say about their investment plans. Third is the stock market’s performance, which is closely tied to that spending. Fourth is layoff activity, because hiring remains soft and a meaningful pickup in layoffs could quickly push unemployment higher and put more pressure on consumer spending.

For now, Basu said, initial unemployment claims remain low — a sign that employers are still largely holding on to their workers. That, he said, “speaks to economic stability.” His conclusion was cautiously optimistic: “My forecast is for growth in 2026.”

That leaves the industry with a message that is neither alarmist nor complacent. Opportunity remains, especially in segments tied to infrastructure, energy and advanced technology. But so do serious headwinds, particularly for projects that depend on easier financing, steadier input costs and broader private demand. That conversation will continue across the industry in the months ahead — including at METALCON 2026, scheduled for Oct. 7–9, 2026, in Orlando. Registration is now open.

Looking for a reprint of this article?

From high-res PDFs to custom plaques, order your copy today!

.webp?height=740&t=1781278983&width=auto "KEE(2).png")